The End of the CAC Arbitrage (?)

The CAC arbitrage that built the last generation of consumer brands is ending. This piece explores what comes next: manufacturing control, niche communities, AI-mediated discovery, and where value accrues when marketing becomes a commodity.

The objective is to frame the problem in a way that helps being directionally right most of the time and to foster a discussion around what may actually be changing under the surface.

1. Death by a Thousand CACs

The last fifteen years in consumer internet were largely driven by a simple dynamic: acquire customers from Meta/Google at x and generate 3x+ in lifetime value. This arbitrage was the long wave of a broader structural shift as discovery and distribution moved online. Intermediaries were removed and a rapidly expanding pool of digital eyeballs was monetized through increasingly efficient advertising.

If we take a step back and look under the hood, what is CAC? In its most simplistic form, CAC is the intersection between how much attention is available (offer) and how many brands are fighting for that attention (demand). Naturally, at brand level, there are dozens of other variables that influence CAC besides demand/offer, but the overall basic idea remains: if you are trying to persuade someone to buy your product, having similar products/companies trying to do the same next to you makes the job harder and more expensive.

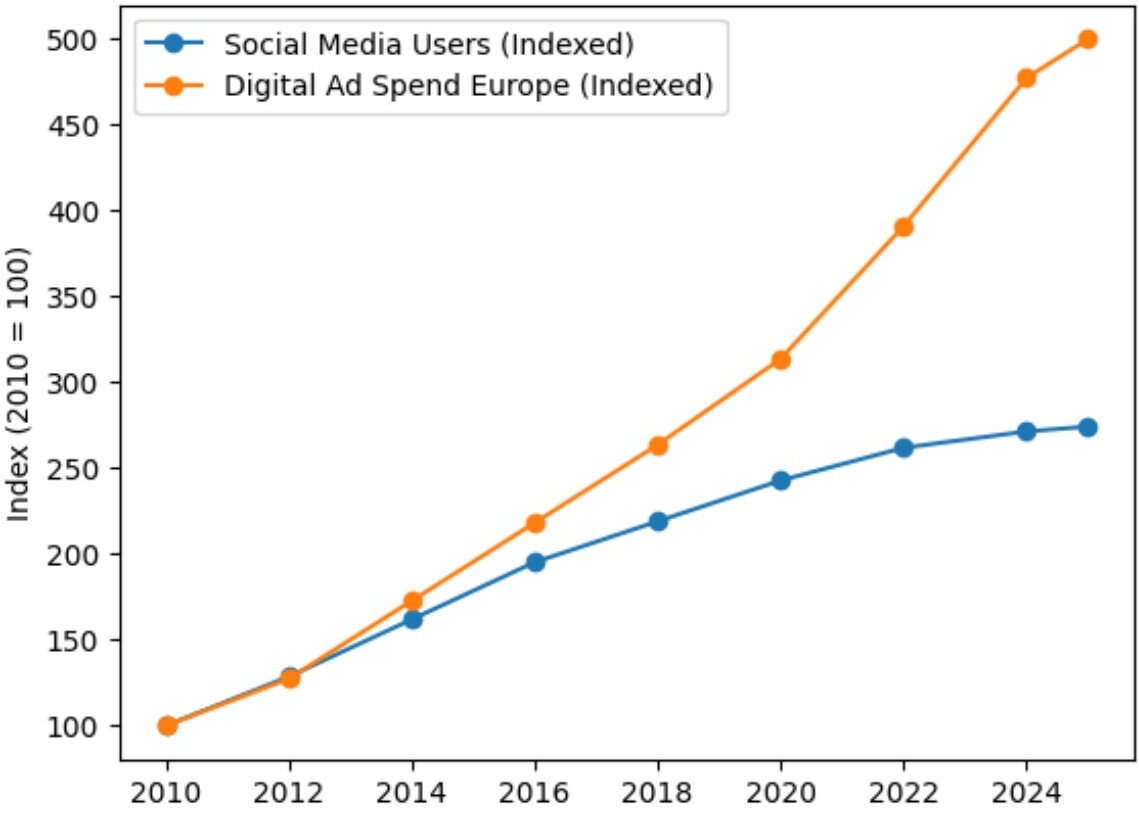

Over the past 15 years, social media adoption in Europe has followed a classic S-curve, with rapid expansion in the early 2010s, steady but slowing growth in the late 2010s, and saturation today. The number of users increased from roughly 200m in 2010 to around 575m in 2025, but the growth rate has collapsed from double digits to low single digits as it reached its natural ceiling. Over the same period, digital advertising spend in Europe grew from roughly €20-25bn to more than €100bn, continuing to compound even as user growth stalled. The divergence marked a transition from a system where attention was expanding to one where brands are increasingly competing for a largely fixed pool of users. In practical terms, competition for attention has structurally increased, putting upward pressure on CAC unless offset by improvements in conversion or targeting efficiency.

Social Media Users vs Digital Ad Spend (indexed) in Europe (2010–2025)

Source: DataReportal (Kepios), Digital Reports (2010–2025), IAB Europe AdEx Benchmarks, Statista

As this shift played out, brands were effectively left with two options: i) outperform with better marketing or ii) look for pockets of demand where competition was still limited but growth strong. In practice, most successful D2C businesses paired execution with favorable category selection.

This dynamic shaped the way the value chain was built, with D2C brands concentrating their efforts on the front end, design, storytelling, and customer acquisition, while outsourcing most of the operational backbone such as procurement, manufacturing, logistics, and returns to third-party partners. The model was coherent in a world where distribution was the primary constraint, while the rest of the system could be modular and "asset-light".

Traditional Fashion Value Chain

Source: Beyond Talent

The real edge, however, was not just access to paid channels, but the ability to move faster than competitors. Winning brands were those that could iterate quickly on creative, test multiple narratives in parallel, and scale what worked. Narrative control and speed of iteration were the core capabilities, more than any individual campaign or channel.

This is where the impact of AI becomes less straightforward than it initially appears. On the surface, AI is being adopted most rapidly in exactly the functions where D2C brands built their advantage, marketing and design. This should, in theory, lower barriers to entry and reduce differentiation by making high-quality creative and optimization accessible to a broader set of players. In reality, AI does not just make things easier, it also accelerates the rate at which the best operators improve. If anything, it may amplify the importance of iteration speed and learning velocity rather than commoditize them. The top players will not simply use AI to do the same things more cheaply, they will use it to run more experiments, converge faster on winning strategies, and personalize at a level that was previously out of reach.

At the same time, it is hard to ignore that the floor is rising as more brands will be able to reach a baseline level of competence in marketing and creative, increasing the number of viable entrants in any given category. The likely outcome is not a uniform compression of differentiation, but a widening dispersion between a long tail of "good enough" brands and a smaller set of operators that continue to compound advantage. The question is whether that advantage still sits primarily in marketing, or whether it shifts elsewhere in the value chain as these tools diffuse.

For the moment it is still background noise, but to understand the direction where things are heading Meta just open-sourced TRIBE v21, a predictive model trained on brain scans of people watching videos, reading or listening to audio. The model potentially allows users to virtually test visuals before launching to cater them to increase conversion and sales2.

In the long-term, value accrues where bottlenecks are: if marketing becomes a commodity, will a D2C brand founded on storytelling be able to maintain a 20-30% profit margin 10 years from now? An important point to add is how in a market with high competition density (like fashion, food, beauty, etc.), a brand does not need a single overperforming competitor to suffer. Increasing competition density by many small up-and-coming competitors can create enough pressure to push down margins and endanger long-term profitability and valuations: death by a thousand CACs.

2. We Are Each of Us Celebrating Some Funeral3

Now that the easy part is done (interpreting the past), the tricky (and fun) part begins (prescribing the future). If (a big if, I am aware) the above interpretation is correct, how do we move on? Where will the value accrue? Most importantly, is it still worth making predictions when so many things change on a daily basis?

Brands are not created equal, in my opinion here are some potential differentiators worth exploring. In my view, investors should gain conviction on at least one of these before backing new consumer brands.

2.1. Manufacturing

I personally see it difficult for an "affordable luxury" brand manufactured in the far-east to be able to command a premium when a plethora of similar brands will suddenly appear on timelines. We've seen some form of it in April 2025, when some "Chinese suppliers" started advertising on TikTok luxury goods made in China but supposedly sold by French/Italian luxury brands at huge mark-ups4. While I doubt it actively had an impact on these brands' performances, probably the truth (as always) sits in the middle and we are likely to see some repercussions from past extensive offshoring in the form of intensified competition. Everyone knows that Chinese factories can make good products cheaply; the difference now is that the information asymmetry that sustained "affordable luxury" is collapsing. Consumers can now see the factory, the production line, the actual cost structure. This is a transparency shock, not only a competition shock, and it means any brand with a large gap between perceived value and actual production cost is exposed, regardless of where it manufactures.

A common theme we therefore hear is that the physical world will regain value: Manufacturing and logistics. Value should accrue where bottlenecks are. Makes sense, no? This is probably too simplistic to be true for the whole market. There is a reason why low-end manufacturing moved to lower wage countries and there is no reason why low value items should be reshored (outside of big macro events, i.e. tariffs etc.). Where is the line? A €30 t-shirt brand cannot absorb this. A €300 handbag brand probably can. A €800 jacket brand almost certainly can.

On the other hand, this will increase value for high-value items that rely on scarcity and hand-crafted curation to command a premium. If marketing becomes less differentiated, the signal of quality shifts from the carrier (creative, storytelling) to the content (materials, provenance, process). Owning production can create differentiation but brands should: i) sit at a price point where increased costs can be pushed through, ii) be able to deliver such messaging and avoid the rift between perceived quality vs actual quality. Brands that can credibly demonstrate why their product costs what it costs will hold pricing power; brands that cannot will face margin compression as cheaper alternatives become more visible. "Out" photoshoots with good-looking models in natural scenarios with a pastel palette; "in" with leather, grains and messaging catered towards craftsmanship and handmade items.

Move from Generic clean color palette to Handcraft visuals

Source: Polène5, Velasca

Moreover, brands that control production can iterate on product faster, manage inventory tighter, and respond to demand signals in near real-time. Zara built an empire on this because owning production meant they could test small, scale fast, and avoid markdowns. Think of Kiton at the extreme end: a brand that controls every step from raw fabric to finished garment, charges accordingly, and is essentially impossible to replicate. Not every brand can be Kiton, but the principle holds: the deeper the production control, the harder the moat to breach.

The implication is straightforward: privilege brands with production capacity or credible paths to vertical integration. Supply chain ownership should move from a "nice to have" to a screening criterion, particularly for any brand above €150 average order value. For companies with externalised production, this is a value creation conversation: can they bring more of the production chain in-house or near-shore? And what does that do to gross margins and inventory turns over the medium term?

2.2. Community

The battle for the plains (large SAMs) is over, now the fight is in the jungles and the mountains (small niches).

For the past decade, social media algorithms have been remarkably effective at homogenizing taste. The same feeds, the same aesthetic references, the same coat, the same "curated" apartment (Ikea has probably been the most underdiscussed winner of the social/reel era). When everyone is exposed to the same inputs and optimized toward the same outputs, the identity signal embedded in mainstream consumption collapses. Wearing the right brand stops meaning anything when everyone is wearing it.

This matters because consumption has always been partly an identity project (do we discover or invent ourselves?). People buy things not just for utility but to signal who they are, or who they want to become. As knowledge becomes commoditized (everyone has access to the same information, the same aesthetics, the same playbooks), the pressure to differentiate shifts from what you know to what you do. People will increasingly look for identity markers in hobbies, sports, subcultures, and communities that are specific enough to feel personal. You will have more and more people joining seemingly random communities (bouldering, ceramics, freediving, ultra-running) not just for the activity itself, but to build a version of themselves that feels irreplaceable.

The structural implication is that niches which were historically too small to support dedicated brands may cross a viability threshold. Not because any single niche explodes in size, but because the long tail of niches collectively thickens. If you have 50 communities each growing from 100k to 500k engaged participants across Europe, that is a lot of new addressable markets opening up at once.

It is very unlikely that there will be a new breakout winner in large generic categories like womenswear or general beauty: the plains have been claimed. But there can absolutely be new winners in the mountains, if we look at markets that would have seemed too small five years ago and accept that the TAM is expanding now.

A potential play in this vertical could be experiences rather than products. Travel is also, not coincidentally, the most popular identity signal in existence. If you experience the unfortunate circumstance of spending time on Tinder/Instagram, every other profile lists "travel, food and cinema" as interests, because they are the easiest categories that fulfill the need to feel unique while requiring minimum effort. Companies that package generic aspirations into specific, social, recurring experiences are monetizing this dynamic in real time.

One caveat worth sitting with: if this thesis is right, it changes what "scale" means for a consumer investor as these brands may never reach €500m in revenue. The question is whether a collection of €50-150m niche leaders with strong margins and low CAC dependency represents a better bet than a single large D2C brand fighting for survival in a commoditizing category. I suspect the answer is yes, but it deserves a proper discussion.

Perhaps Rapha is not dead yet? Rapha6 may be the perfect illustration of how a brand can suffer death by a thousand CACs (growing competition from the long tail of cycling apparel brands all running decent Meta campaigns) while simultaneously holding the answer in its hands: a genuinely loyal community, deep niche credibility, and a product layer that extends from gear to experiences to content. If the thesis in this piece is right, Rapha's niche appeal is an asset (not a liability) and the question is whether it can lean into community hard enough to outrun the margin compression from commoditized competitors.

2.3. Distribution

If differentiation in marketing compresses, control over how and where products reach consumers becomes a more important lever. There are three dimensions worth separating.

The first is channel breadth. The brands most exposed to CAC inflation are those with 70%+ revenue concentration on a single paid channel: the same brands that were celebrated for their "DTC-native" efficiency five years ago are now structurally fragile because they never built alternative routes to market. The winners going forward will be brands that can sell across their own e-commerce, wholesale, marketplace, and physical retail without losing brand coherence. This is operationally hard and requires real capability (what a moat in the end is).

The second dimension is physical retail, which deserves a re-evaluation in this context simply because digital became worse (more expensive, more competitive, lower-converting). A well-placed store is a customer acquisition channel with zero marginal cost per impression and conversion rates that no paid digital funnel can match. The brands we should look at most seriously are those treating retail as a margin-accretive acquisition tool. This requires sitting with the uncertainty of attribution: the correlation between store investment and measurable sales is indirect, and that discomfort keeps many digital-native brands from making the leap.

The third dimension, and potentially the most disruptive one, is the emergence of AI-mediated commerce. This connects to the GEO discussion below, but the core point is: if a meaningful share of purchase decisions shifts from "I saw an ad on Instagram" to "I asked an AI assistant what to buy," then the entire acquisition model changes. The brand does not need to win an auction for your attention. It needs to be the answer when an agent is asked a question. This is a fundamentally different game, and almost nobody in the consumer brand ecosystem is thinking about it seriously. There is also a more extreme scenario worth considering: what happens when AI agents start making routine purchases on behalf of consumers? "Reorder my shampoo," "find me a cheaper alternative to X." In categories where loyalty is shallow and switching costs are low, this could erode brand preference entirely. The brands most at risk are those that rely on habit and visibility rather than genuine product differentiation.

2.4. Taste (?)

This is the hardest thesis to underwrite because it is the hardest to measure, but it may be the most durable source of differentiation in the coming cycle.

AI can generate: i) a competent brand identity, ii) a decent lookbook, iii) a functional product page. What it cannot do, at least not yet, is have a genuine point of view. Taste, in the way that matters for premium consumer brands, is an editorial function: the ability to say no to most things and yes to a specific, coherent few. It is what separates Aesop from another "clean beauty" brand, or Jacquemus from another "Mediterranean-inspired" fashion label.

The argument is simple. As execution becomes cheaper and more accessible, the scarcity shifts upstream to curation and creative judgment. Brands built around a founder or creative director with a distinctive and consistent vision may become more valuable, not less, precisely because they possess something that AI makes harder to fake.

This thesis can become self-serving very quickly: every founder believes they have taste, most of us have no taste (despite a similar receding hairline, I ain't Rick Rubin). The practical filter should be to look for brands where product and creative decisions are opinionated and consistent over time, and where the customer base responds to the brand's identity rather than just its price or convenience. High NPS, pricing power above category, and low discount dependency are all proxies. If a brand needs to run 40% off promotions to move inventory, whatever "taste" the founder claims to have is not translating into willingness to pay. This is clearly easier to spot ex post rather than ex ante, I genuinely question whether any of us have what it takes to make these value judgments.

A related risk: taste is inherently founder-dependent, and founder-dependent brands carry key-person risk. This does not make them uninvestable, but it changes how investors should think about risk protection.

3. "So What?"

3.1. Meet GEO, the New SEO

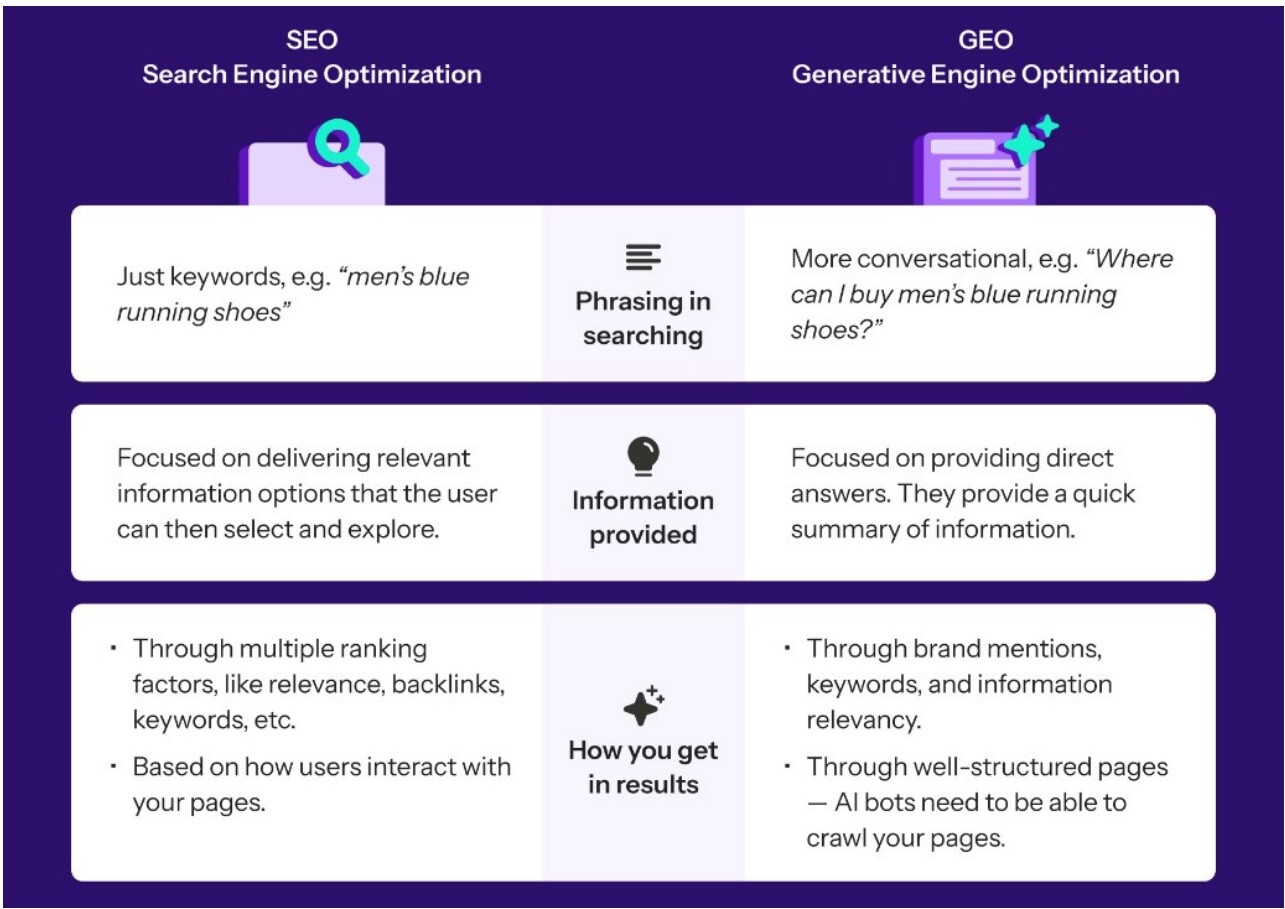

If AI assistants become a meaningful discovery channel, the rules of the game change. Today, when a consumer asks ChatGPT or Perplexity "what is the best weekender bag under €300?" or "what skincare brand is good for sensitive skin?", the answer is not (yet) shaped by ad spend. It is shaped by the brand's presence across training data, reviews, editorial mentions, Reddit threads, and structured product information. In other words, the output is a function of whether the brand is genuinely well-regarded across the internet, not whether it has a large Meta budget. This is a fundamentally different acquisition surface than a feed, and it inverts the logic that most D2C brands were built on. Being "recommended by the algorithm" matters less than being "known to the model."

SEO vs GEO

Source: SEO.com

The practical question for companies is simple and somewhat uncomfortable: when someone asks an AI "what is the best [category] brand for [use case]?", does your brand appear? Most D2C brands have no idea how they show up (or whether they show up at all) in AI-generated recommendations, and almost none are actively optimizing for it. This is an emerging capability gap that naturally favors brands with strong organic presence, high-quality reviews, and editorial coverage.

I would not overstate the urgency here: this will not matter next quarter, but within two to three years, it could represent a material share of discovery in categories where consumers actively research before buying (considered purchases, premium goods, anything health-related). The brands that start building this presence now will compound an advantage that will be very difficult to replicate later.

There are concrete steps companies can take right now, and the first movers will have a significant edge because so few brands are thinking about this. AI models parse structured, well-written content far more effectively than they parse ad copy or Instagram captions. Companies should invest in organic community building that generates genuine discussions between followers, because those conversations feed the training data and review corpus that models draw on. They should start writing detailed blog posts that directly target consumer questions: "best moisturizer for dry skins in 2026", "how to choose a barefoot shoe for beginners." This is not SEO in the traditional sense; it is about creating the kind of clear, authoritative, question-and-answer content that AI models love to surface. Reddit is particularly important here, as models are extensively trained on Reddit data and a genuine brand presence there (not astroturfing, but real engagement) can materially influence how a brand appears in AI recommendations. If companies do this well while competitors remain focused on paid acquisition, the competition will not know what hit them.

3.2. Buy vs Build

When assessing a fashion brand, one of the clearest differentiators between an up-and-coming brand and an established one is how they think about marketing spend. LV does not discuss CAC: for LV marketing is brand maintenance to remain top-of-mind, not to explain to people who they are. The implication is that established brands will suffer relatively less from the structural cost increases described above, because they are not fighting to build mental real estate from scratch as they already own it.

On the other hand, what was a viable (and cheap) way to create a new brand over the last 15 years, the CAC arbitrage, is no longer available on the same terms and we should not expect a new Sézane to arise from the old playbook. The market seems not to have fully priced this. Up-and-coming brands are still trading at 2-4x sales, while established listed brands trade at 12-14x EBITDA (1-2x sales). Part of this is a function of different growth trajectories, but the premium embedded in emerging brand multiples assumes future customer acquisition efficiency that the structural CAC shift directly challenges. It is not that growth will not happen, but the cost of delivering that growth may be permanently higher than the multiples assume, compressing the margin expansion that justifies the premium.

A clever eye will ask: "does this mean there is an opportunity to invest in undervalued established brands? And how does this reconcile with the earlier discussion on community?" The nuance is important: not all established brands are undervalued. An established fashion brand at 12-14x with no community, no manufacturing control, no taste beyond legacy recognition, and no GEO presence is not cheap, but correctly priced for slow decline. The opportunity lies in established brands that possess at least one of the structural advantages described above: production control, embedded community, genuine taste, or distribution breadth. These are the brands with real mental real estate and a defensible reason to keep it.

3.3. CAC Is Higher, What About LTV?

So far this piece has been entirely about acquisition costs, which is a blind spot worth flagging. I am completely missing how you can extract more value per customer relationship over time. AI's impact on retention, repurchase, and personalization could matter as much or more than its impact on creative production, and it is the area where the discussion is least developed. A brand that uses AI to genuinely personalize the post-purchase experience (better product recommendations, smarter replenishment timing, fit prediction, proactive service) could see LTV expand enough to absorb structurally higher CAC. The broader point is that the threat from AI sits primarily on the acquisition side of the equation (more competition, lower creative differentiation, rising costs) while the opportunity from AI sits primarily on the retention side (deeper relationships, better personalization, higher repurchase rates). Brands that use AI to deepen relationships with existing customers can widen the moat rather than see it eroded. If this is correct, it changes how we should evaluate brands: specifically whether a brand has the data infrastructure, customer relationship depth (and the willingness) to use AI on the retention side as aggressively as competitors are using it on the acquisition side.

For established companies, this should become an active board-level conversation rather than something they leave to the marketing team. If the answer to "What are you doing with AI" is "nothing" or "we are exploring it," that is a value creation gap they should close. For some companies this will mean investing in infrastructure, for others it will mean hiring differently: fewer performance marketers, more people who understand customer data, product recommendation systems, and automation. A brand that has no thesis and no curiosity about how AI could reshape the consumer experience is telling us something about how it thinks about the world. Not every company should have a fully built AI personalization stack, but they need to recognize that the game is shifting and they should be actively experimenting. Brands that do not embrace uncertainty will struggle to exist in 10 years: "In a world of rolling shocks, winning companies treat strategy as a dynamic set of bets that evolves with new signals"7.

This section deliberately stays high-level because the LTV side of the equation deserves its own dedicated analysis. The dynamics are fundamentally different across categories (replenishment-driven BPC vs. fashion with seasonal purchasing vs. food with daily frequency), and the data infrastructure requirements vary accordingly. This piece frames the problem. The opportunity side deserves equal depth, and I may explore it separately.

4. Conclusions

I have no crystal ball, everything in this piece could be wrong, or early, or both. AI could lower CAC faster than it raises the floor, niche communities could turn out to be a mirage, and taste could be a post-hoc rationalization that only looks like a moat in the rearview mirror.

But here is what I keep coming back to: the system that produced the last generation of consumer brand winners (cheap attention, efficient paid acquisition, modular and asset-light operations) was not a permanent state of the world. It was a window that opened when social media adoption was expanding and digital ad markets were still underpriced, and it closed when attention plateaued but competition for that attention did not. Most of the playbook that worked between 2012 and 2022 was a product of that specific window, not a timeless truth about how brands are built, and I think we collectively spent too long assuming it was the latter.

If that interpretation is correct (a big if, as always), the next generation of winners will look different from what we are used to seeing. They will own more of their supply chain, not because reshoring is fashionable but because production control is one of the few sources of differentiation that AI cannot replicate. They will be embedded in communities rather than selling to demographics. They will treat discovery as something earned through genuine quality and organic presence rather than something bought through an auction. And they will use AI not primarily to acquire customers more cheaply, but to understand and serve the ones they already have.

None of this means the old brands are dead, some will adapt and a few will thrive precisely because they already have the mental real estate that new entrants can no longer buy cheaply. But the brands that were built entirely on the arbitrage, with no structural advantage beyond knowing how to run Meta campaigns, are the ones whose funeral we are attending. The question for operators and investors alike is whether you are clinging to the old reality or looking for opportunity in the new one.

Baudelaire would tell you the answer is obvious. But then again, he died broke.

Thanks to Igor Pezzilli for the mentorship and the inputs that sharpened this piece considerably.

1 ↩ Introducing TRIBE v2: A Predictive Foundation Model Trained to Understand How the Human Brain Processes Complex Stimuli

2 ↩ f*ckgrowth on X: "how to predict v*rality"

3 ↩ Baudelaire, "On the heroism of Modern Life". Modern society is "an immense cortège of undertaker's mutes" all dressed in the same black coat. The point was that clinging to the past is wrong: the task is to find opportunity in the new reality, not to focus on the old one.

4 ↩ How Chinese factories are quietly destroying the luxury brand image? | by Elvis Hsiao | UX Collective

5 ↩ Of course Polène remains a spectacular brand – maybe I chose their photo just because they have been "too successful" in their marketing and costed me too much over the years 🙂

6 ↩ Rapha appoints high-achieving board director to help drive next phase of growth - FashionNetwork

7 ↩ Bain & Co, internal newsletter

Comments

Sign in to join the conversation

Sign In