AI with a Side of Fries

AI has become the dominant investment narrative, but food retail continues to offer stable, resilient returns supported by real economics rather than narrative momentum.

AI has become the dominant investment narrative, and capital is reallocating at a speed we haven't seen since the early internet cycle. The problem is that narratives can distort the underlying economics of entire sectors. AI will transform many parts of the value chain, but it won't fundamentally change demand patterns in categories where consumption is non-discretionary and behaviour is stable. Food retail is one of those categories.

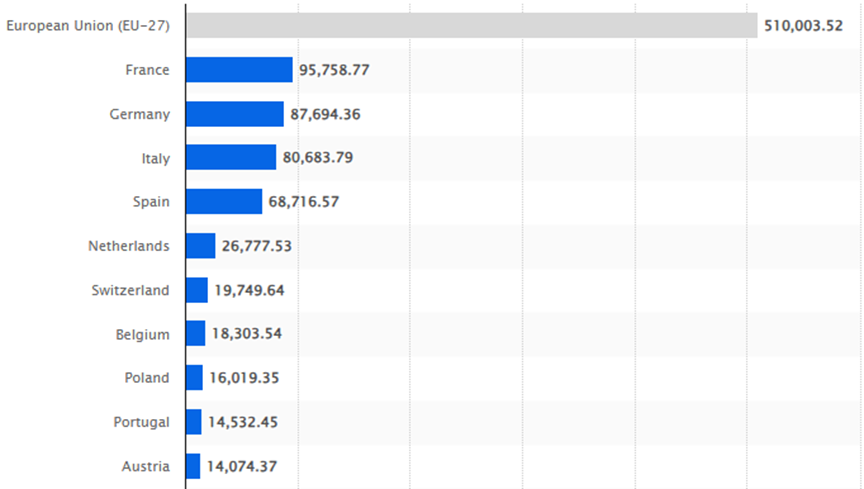

In 2023, the EU food and drink service industry generated €510bn in net turnover across 1.55m establishments, growing even after years of inflationary pressure and supply chain volatility. Central and Eastern Europe posted the strongest growth (+5 to +10 percent), Southern Europe remained slightly positive, and Western Europe hovered around flat performance. This is not a sector driven by explosive cycles, but one defined by consistency.

Top 10 Countries by Net Turnover in the F&B Service Industry in Europe in 2023

Source: Statista, Eurostat

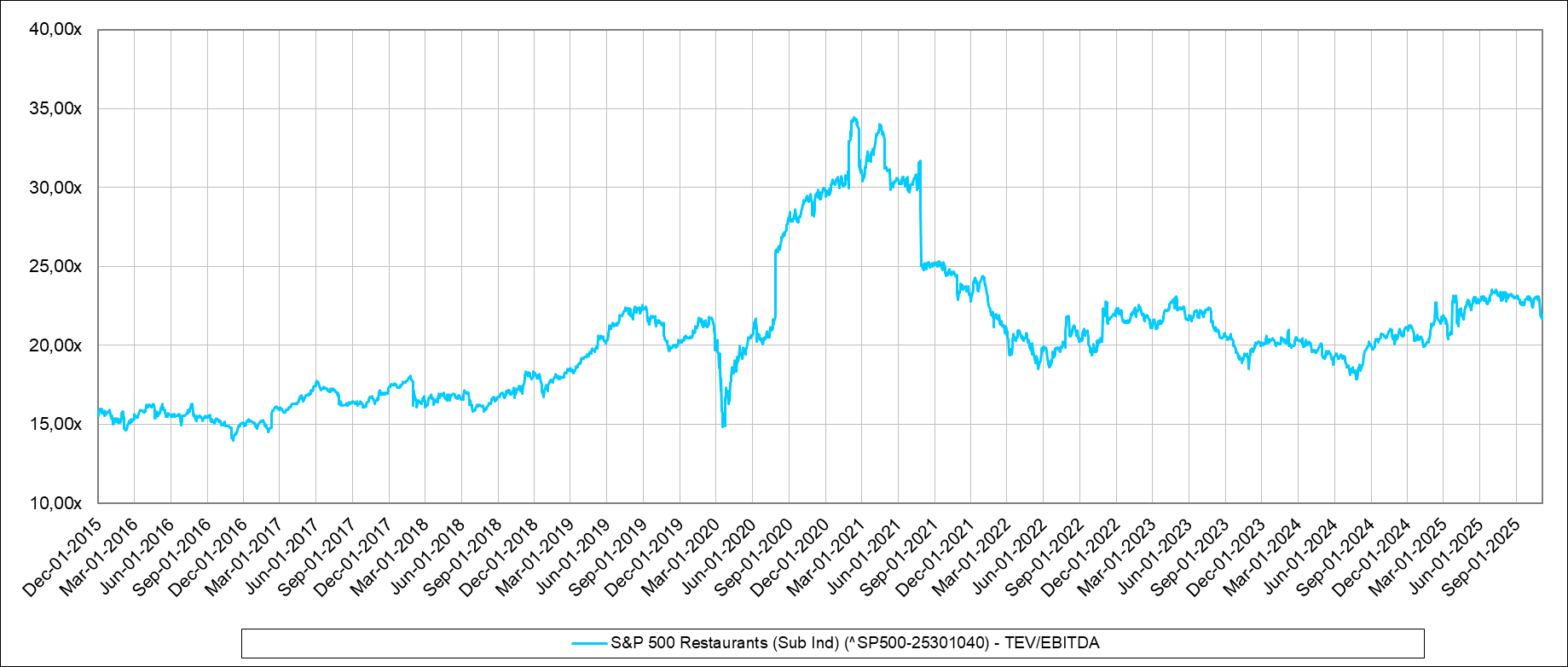

From an economic standpoint, the industry remains one of the most attractive in consumer. Mature operators typically deliver 20–25 percent Ebitda margins at the store level, which is remarkable in a category many investors overlook. Public comps reinforce the same pattern, trading between 20 and 25 times Ebitda for six consecutive years despite COVID disruptions, labour shortages, rising food costs, and shifts in delivery behaviour. It's rare to find this level of multiple stability in consumer retail.

Last 10 years TEV/EBITDA (NTM) multiple evolution S&P 500 Restaurants

Source: S&P Capital IQ

So why isn't capital flowing here? Because investor memory is short. Over the past decade, consumer investing suffered from a simple imbalance: capital inflows outpaced actual returns. Too many DTC brands raised money at unjustifiable valuations, and the failures left a negative halo over the entire category. The instinct now is to avoid consumer altogether, even though restaurants have very different economics from the asset-light, high-CAC DTC model that dominated the previous cycle.

This can create an interesting setup as fundamentals remain strong, cash flow is predictable, unit economics are well understood yet competition for deals is lower than it has been in years. In other words, it is not a contrarian bet that requires a heroic thesis. It is simply a rational allocation decision at a time when attention has shifted elsewhere.

Within the Category, Three Segments Stand Out as Structurally Attractive

Healthy fast-casual continues to expand due to clear consumer shifts toward lighter, nutritionally transparent meals. The GLP-1 effect accelerates this dynamic as consumers reduce portion sizes and alcohol consumption. These formats already operate with modular menus, high throughput, and efficient paybacks, so the growing demand is additive, not disruptive.

Modern takes on evergreen categories such as bakeries and cafés are quietly building some of the strongest unit economics in the space. They operate on high frequency, multi-daypart demand, and premium positioning built around quality. These are not speculative models. They are operationally disciplined, repeatable, and often underestimated by generalist investors.

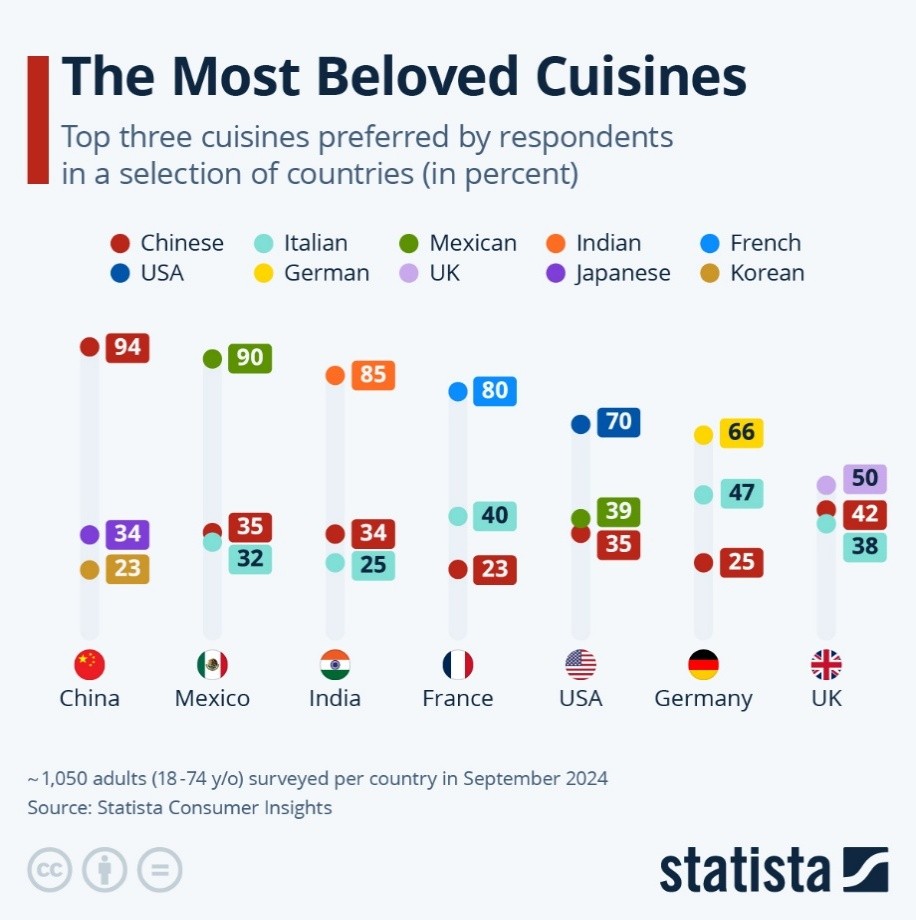

Ethnic and globally inspired concepts outperform because they combine authenticity with scalability. They benefit from menu overlap, high perceived value, and the ability to maintain pricing power even through inflationary cycles.

Favorite ethnic cuisine by country - Beloved Cuisines

Source: Statista Consumer Insights, ~1,050 adults (18-74 y/o) surveyed per country in September 2024

AI will influence the sector in practical ways. Automation will reduce labour intensity, ordering will become more efficient, and supply chains will rely more on predictive systems. But these shifts enhance margins rather than redefine the category. The core drivers remain the same: location, consistency, replicability, and brand relevance.

In a market where capital is chasing AI with increasing concentration, the opportunity may be in the places where the fundamentals are stable and competition has thinned. Food retail fits that description. The industry won't deliver exponential growth curves, but it will deliver something that has become rare: steady, resilient returns supported by real economics rather than narrative momentum. This could easily be the best moment in a decade to invest in the space. Not because it is misunderstood, but because it is being ignored.

Comments

Sign in to join the conversation

Sign In